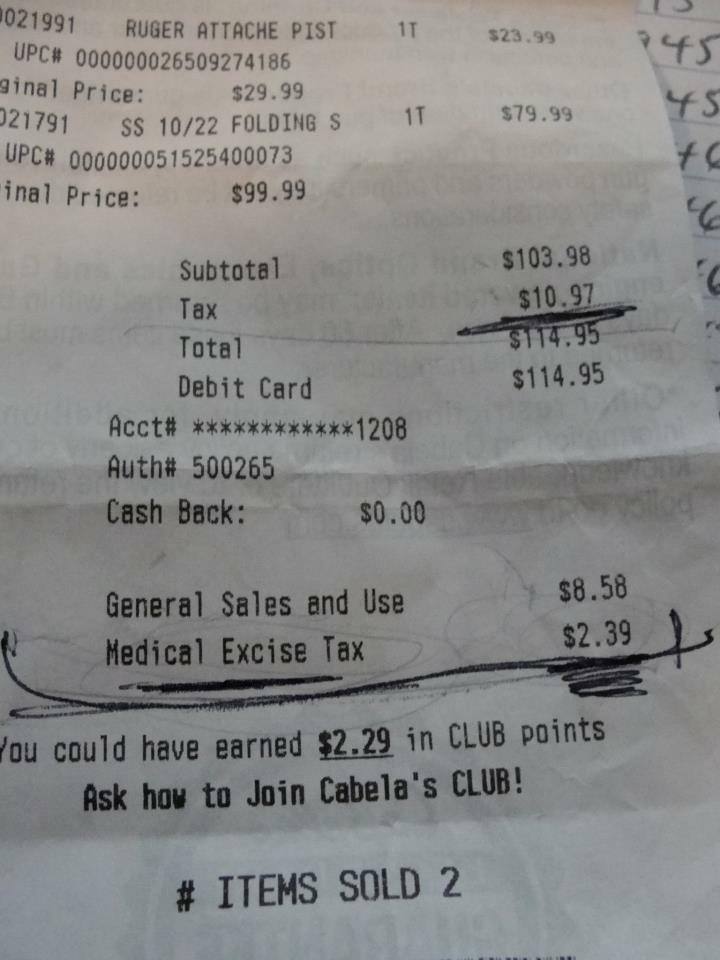

Claim: "Obamacare" provisions imposed a 2.3% excise tax as of 1 January 2013.

| TRUE: Health care legislation imposed a 2.3% excise tax on the sale of medical devices as of 1 January 2013. |

| TRUE: The Cabela's chain (and some other stores) mistakenly applied medical excise taxes to some non-medical purchases made on 1 January 2013. |

| FALSE: The medical excise tax applies to non-medical items such as archery and sport fishing equipment, tires, coal, and "gas guzzling" automobiles. |

Example: [Collected on Facebook, January 2013]

OK.... Here comes some of those Obama care taxes on

Let the ObamaCare fun begin! Clothing now counts as being taxed under the ObamaCare because it "alters the function of the body" See blurb below. I wish more companies would have the balls to do it the way Cabella's is, but most will bury it the cost of the product.

The new law provides that any device defined in §201(h) of the Federal Food, Drug, & Cosmetic Act (FFDCA) that is intended for humans will be taxable. The FFDCA is written very broadly to include instruments, machines, implants and in vitro reagents, among others. §201(h) also includes associated parts and accessories, which are

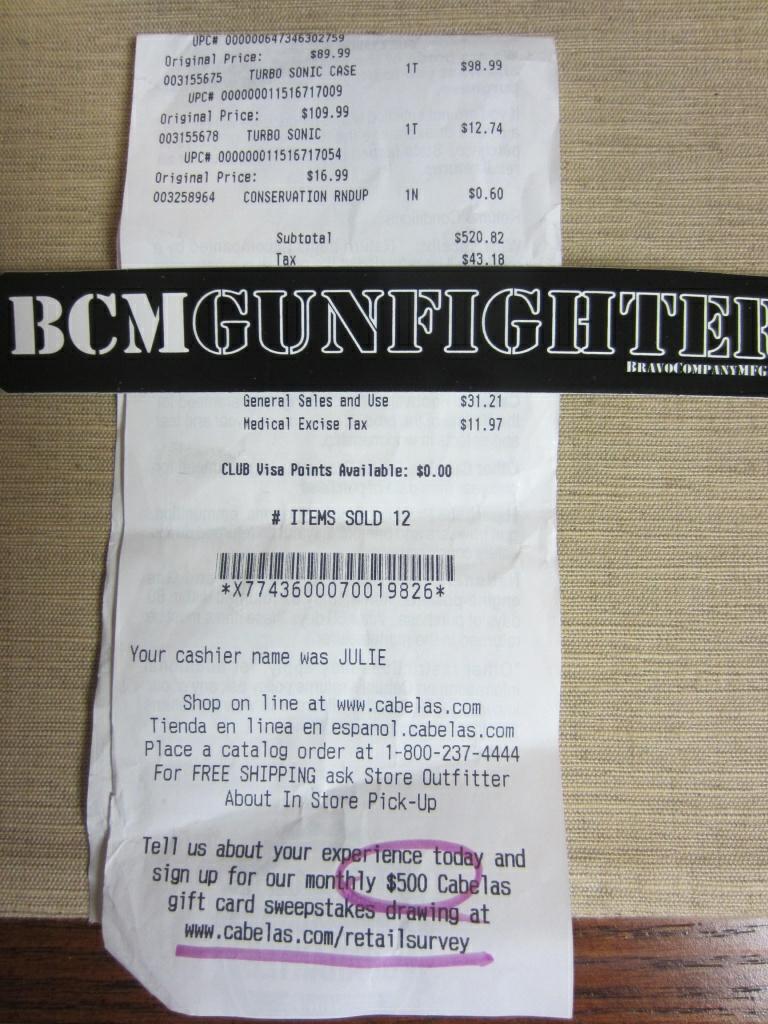

Included is a copy of a Cabela's receipt that charges a Medical Excise Tax of $11.97. This is what the guy said he bought:

3 pair of hiker socks

2 safe door pocket organizers

1 pair female boots

1 female jacket

1 female workout pant

1 Lyman sonic brass cleaner

The receipt total was $520.82. 2.3% of that is

................................ drum roll please

.......................................... $11.97.

Origins: One of the provisions in the reconciliation bill (HR 4872) passed in conjunction with the Patient Protection and Affordable Care Act (PPACA) health care legislation, also known as "Obamacare," instituted a

tax

on the first sale of medical devices as of

The text of the legislation states that the roster of “taxable medical devices” does not include "eyeglasses, contact lenses, hearing aids, and any other medical device determined to be of a type that is generally purchased by the general public at retail for individual use."

Anticipating what constitutes a "taxable medical device" under this legislation can be rather confusing, as explained in a July 2012 tax adviser article.

(1) Recognized in the official National Formulary, or the United States Pharmacopeia, or any supplement to them; The device must also “not achieve its primary intended purposes through chemical action within or on the body of man or other animals” and not depend “upon being metabolized for the achievement of its primary intended purposes.” Sec. 4191(b)(1) limits the definition for purposes of the tax to devices intended for humans. Under what is commonly called the “retail exemption,” the tax provision does not apply to eyeglasses, contact lenses, hearing aids, and any other medical device determined by Treasury to be of a type that is commonly purchased by the general public at retail for individual use.

Under Sec. 4191(b)(1), a taxable medical device is a device, as defined in Section 201(h) of the Federal Food, Drug, and Cosmetic Act (FFDCA) (21 U.S.C. §321(h)), that is intended for humans. The latter provision defines “device” as an “instrument, apparatus, implement, machine, contrivance, implant, in vitro reagent, or other similar or related article” — including “any component, part, or accessory” — that meets certain requirements. The device must be:

(2) Intended for use in the diagnosis of disease or other conditions, or in the cure, mitigation, treatment, or prevention of disease in man or other animals; or

(3) Intended to affect the structure or any function of the body of man or other animals.

According to proposed regulations issued by the Internal Revenue Service in February 2012, the medical items that would be exempt from the tax because they are "commonly purchased by the general public at retail for individual use" should be determined as:

The following factors suggest that a device is of a type that is regularly available for purchase and use by individual consumers who are not medical professionals: (A) Consumers who are not medical professionals can purchase the device through retail businesses that also sell items other than medical devices, such as drug stores, supermarkets, and similar vendors.

A device will be considered to be of a type generally purchased by the general public at retail for individual use if it is regularly available for purchase and use by individual consumers who are not medical professionals, and if the design of the device demonstrates that it is not primarily intended for use in a medical institution or office or by a medical professional.

(B) Consumers who are not medical professionals can use the device safely and effectively for its intended medical purpose with minimal or no training from a medical professional.

(C) The device is classified by the FDA under

(Physical Medicine Devices).

Why the medical device excise tax should have been applied to all the items listed in the receipts pictured above was something of a mystery to viewers when these images were originally circulated back in January 2013. Although some states

allow sellers to pass along the expense of the new medical device excise tax to customers by "separately stating a line item charge on the invoice or receipt given to their customers for 'Federal Excise Tax' or something similar,"

the vendor in this case, Cabela's, is a retailer of hunting, fishing, camping and related outdoor recreation merchandise not known for selling medical devices, and the items listed in the receipts (such as a Ruger Attache Pistol Case) would not seem by any stretch of the imagination to fit FDA definitions of medical devices.

The answer was that vendors typically use upgraded sales software at the beginning of each year which is programmed to handle changes in tax laws that have just gone into effect, and on

The error was discovered last week after consumers in several states notified the company that the surcharge appeared on their sales receipt and had been applied to all of their purchases. "It was a glitch in the system,” said Cabela's spokesman Joe Arterburn said. The error was limited to transactions that occurred Jan. 1 and was caught that same day by the Sidney, Neb.-based hunting and outdoor outfitter. Images of Cabela's sales receipts showing the surcharge have appeared on various websites prompting several rumors. One rumor alleged that retailers had begun passing their employees' insurance coverage costs onto consumers in the form of a medical excise tax. Other sites claimed that because the tax had been applied to shoes and shirts that clothing and footwear are now considered medical devices under the new law. Both speculations are false.

A companywide glitch in Cabela's cash register system that added a 2.3 percent “Medical Excise Tax” to customers' purchases — everything from boots to bullets — was an error and will be refunded, a company spokesman said.

Some readers have incorrectly interpreted the listing of federal excise taxes on forms of sport fishing equipment, archery equipment, tires, coal, and gas guzzlers in

Last updated: 28 June 2013

Sources: |

Podsada, Janice. "Cabela's Blames 'Glitch' for Jan. 1 Tax Error, Promises Refunds." Omaha World-Herald. 8 January 2013.